Swiss online consumption to grow by 3 percent in 2023

Together with GfK Switzerland and in collaboration with Swiss Post, the Swiss Retail Association.swiss has conducted the overall market survey for online retail in Switzerland. Online retail in Switzerland is set to grow by 3 percent in 2023 (including abroad).

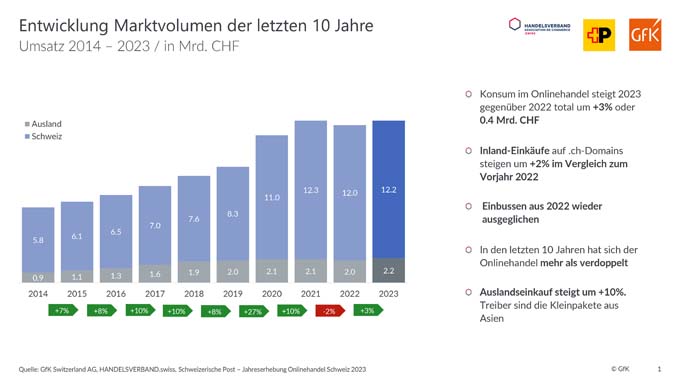

In 2023, online retail was able to make up for the losses from 2022 and is back at the sales level of 2021 with a total of CHF 14.4 billion. In the last 10 years (2014 to 2023), online sales have more than doubled, from CHF 6.7 billion in 2014 to CHF 14.4 billion in 2023. Online shopping abroad has reached a new high of CHF 2.2 billion and is growing by 10% compared to 2022. This is being driven by small parcels from Asia.

How much was purchased?

In 2023, goods worth 14.4 billion Swiss francs were ordered online by private individuals in Switzerland, of which:

- 2 billion Swiss francs directly from retailers in Switzerland (purchase in Swiss francs incl. VAT).

- 2 billion Swiss francs directly from dealers abroad.

In contrast to the previous year, the distribution of sales in the months was very balanced. Only June 2023 saw above-average growth compared to the other months. However, this trend did not continue in the second half of the year, meaning that the year ended with an increase of just 3% compared to the previous year.

The online share of the overall non-food market has also recovered and now stands at 18.8%. The online food share has fallen to 3.0 percent

What is ordered in Switzerland?

For retailers whose main product range is home electronics, 53% of sales are generated online. Another increase compared to the 52% in 2022. Sport has recovered to an online share of 27%, similar to 2021. In the fashion/shoes segment, 28% of purchases are made online, in the home & living segment around 17%. The sector distribution still shows the predominance of home electronics with 24% and fashion/shoes with 17% of the total online market. Followed by Home&Living with 13% and Food with 11%. Universal mail order companies are below the 10 percent mark with 7 percent and sports with 5 percent. Books/Media, Health&Beauty and DoIt each share the 3-4% share.

Loser and winner sectors in 2023

Different sector trends can be observed: Fashion/shoes lost -7% and home electronics -5% compared to the previous year. The majority of the sectors are flat, with only the sports and food sectors increasing by 6%. This means that food is ahead of non-food, with the home electronics and fashion/shoes sectors lagging behind. Marketplaces and portals are also among the winners this year.

Increasing foreign purchases / direct imports

Online shopping abroad has reached a new high of 2.2 billion Swiss francs and is growing by 10 percent compared to 2022. This is being driven by small parcels from Asia. These are mainly delivered directly to Zurich and Geneva by air freight by the major platforms.

Preferred purchasing channels

The study results show that consumer preferences will continue to shift towards "online" in 2023. Compared to 2019 and 2022, they are increasingly making "hybrid" purchases. The increase is particularly visible in the sports and home & living sectors. Omnichannel has become a necessity.

Post Covid conclusion

The new "normal" shows that habits from the Covid era have not completely returned and that certain sectors continue to enjoy great popularity in e-commerce. However, 2023 also shows that special purchases during the pandemic cannot be repeated at will, and that industries have had to deal with high stock levels and help themselves with sales.

Outlook 2024

The authors of the study assume that online consumption will continue to grow in the low single-digit percentage range in 2024 and that consumer sentiment will not improve until 2025. The dominance of marketplaces and portals will continue to grow, but could face increased competition from abroad. In the retail sector, we will see further consolidation both in the retail space and in traditional mail order. Social commerce will play an increasingly important role, particularly among Generation Z, and this will add further purchasing channels for retailers. Consumers will increasingly shop according to the motto "here and now - whether stationary or online".

Source: www.gfk.com