Swiss payment traffic: What does the future hold?

With the QR bill, which will definitively replace the old payment slips on October 1, 2022, the Swiss financial center is venturing a step into the future. The QR-bill is a "chicken and egg" solution that meets the needs of both nostalgic switch lovers and those who have long since taken the step into the world of digital payment transactions. This is a good time for QR Modul to take a look at the possible future of Swiss payment traffic.

In the last 10 years or so, numerous new providers have emerged in the payments market. A field of finance that was once considered "dusty" has changed dramatically thanks to new technologies, especially mobile, e-banking and online shopping. Innovative fintechs are competing for a share of the pie, which offers great potential with over one billion bills sent in Switzerland alone (source: SIX Group AG). In addition, there are the transactions at the store checkout, in the restaurant and in online shopping. While QR billing solution providers and eBill network partners are vying for the classic billers, relatively young providers such as TWINT, Apple Pay, Samsung Pay and others are fighting against the classic debit and credit cards. It seems like there is now a dedicated solution for every conceivable instance where money is moved from one person to another. The only question is: Who can still keep track of it all? Is it even worth maintaining so many parallel infrastructures? One thing is clear: in the end, the end customers pay the price.

QR code serves analog as well as digital payment transactions

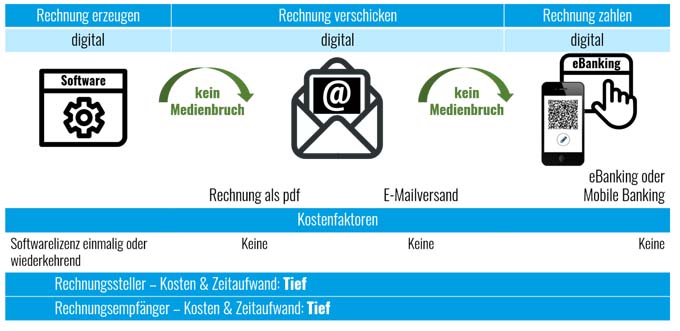

With its entry into digital payment processing, the QR bill ventures out of the analog world of payment slips and significantly improves the convenience of digital payment. In particular, the option shown in the figure of being able to pull a QR bill in pdf format directly into eBanking, thus preventing media disruptions, represents an important milestone. This makes the QR bill the only procedure that can efficiently serve both the analog and digital worlds, which means that billers must ask themselves whether they are giving away too much leeway at best by switching to a purely digital channel such as eBill.

Instant payments will change old habits

If one additionally takes into account that interbank payment traffic in Switzerland will soon offer the possibility of processing payments in real time, further thought games suggest themselves. Because, as SIX Group Ltd already communicated in September 2021, it is planning to introduce "instant payments" in August 2024 together with the Swiss National Bank. When bank-to-bank payments are processed in real time, the bill recipient receives the credit note within seconds after the payer has triggered it in his mobile or eBanking app. As a result, this type of transaction could also become interesting for retailers - both in stores and online. After all, if a retailer writes QR invoices in certain cases anyway, what would be the argument against using the Swiss QR Code at the store checkout as well? The customer would pull out his smartphone, scan the QR code and release the payment. The merchant would receive the confirmation of receipt immediately - similar to TWINT, Apple Pay, Samsung Pay, etc., but without a detour via a third-party provider who takes a share of the revenue for himself. Why should the merchant then still maintain these payment methods if all transactions could be processed via a single standard, the QR bill?

Competition promotes innovation, but also complexity

The future will show where the journey is headed. On the one hand, it leads to more innovation when different providers compete against each other. On the other hand, x-different infrastructures not only increase complexity, but also costs for billers. Particularly in an area such as payments, where a single but omnipotent infrastructure would be perfectly adequate, the question arises as to which service will bring the most benefit to the parties involved. It remains to be seen whether the various providers that are already available and that will enter the market in the future will be able to hold their own, or whether the trend will move back toward the elegant simplicity of a single standard. If the latter is the case, the exciting times in the payment traffic market could soon be over and the bland stability of the past decades would return. In return, payment traffic would once again be clear and predictable.

Author:

Beni Schwarzenbach is Managing Director of QR module.