Private banking sector is on the move

The private banking sector is moving, but it is under severe pressure: The number of private banks operating in Switzerland fell from 101 to 96 in 2020 by the middle of this year. This is shown by the latest private banking study by KPMG and the University of St.Gallen (HSG).

In the annual "Clarity on Performance of Swiss Private Banks" study, KPMG and the University of St. Gallen (HSG) examined a total of 83 private banks operating in Switzerland and assessed the performance of these institutions as well as key industry trends. In addition, 250 statements on the situation of the banks during the pandemic were scrutinized and 27 executives - mainly CEOs - from the private banking sector were interviewed.

Challenging environment

The environment for the private banking sector remains challenging, even though many institutions initially came through the corona crisis well, concludes the private banking study by KPMG and the HSG. According to the study, small private banks with assets under management of less than CHF 5 billion are particularly affected. Their turnover slumped by around 13 percent in 2020. Low interest rates are the main factor depressing earnings. At the same time, small private banks are increasingly reaching their limits in terms of digitalization and due to the increasing density of regulation. As a result, and driven by high margin pressure and the need for economies of scale, consolidation is continuing.

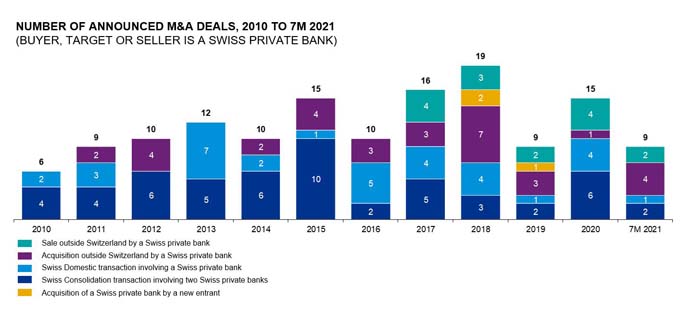

Private banking sector continues to shrink

This is reflected not least in the sharp increase in M&A activity since the first lockdown: eight consolidation deals were announced between July 2020 and July 2021. At the same time, the number of private banks operating in Switzerland has decreased from 101 to 99 in 2020. Currently, there are still 96 private banks in Switzerland - and after the completion of the transactions already announced, there will likely be 93. "In our view, there is still a great need for consolidation, especially among smaller and medium-sized private banks," said Christian Hintermann, banking expert and partner at KPMG Switzerland. "We therefore expect transaction activity to remain high over the next twelve months. In addition, we expect the number of private banks in the Swiss market to decrease by another quarter in the medium term." Over the past ten years, the number of institutions in Switzerland has already declined by 40 percent (158 private banks in 2011).

Gap between large and small private banks widens further

What is striking in the private banking sector is that the gap between large and small banks widened even further last year: Large institutions performed better than medium and small banks in 2020 and proved more resilient to the challenges of the pandemic. In fact, they were even able to slightly increase their 2020 sales (+0.8%) despite difficult circumstances, while medium-sized private banks suffered a sales decline of 7.2% and small institutions even suffered a sales slump of 12.8%.

A look at the cost/income ratio also clearly shows the differences: while the large private banks were even able to improve it slightly (74%), the cost/income ratio at the small private banks rose by 10 percentage points to 95%, the highest value in the last five years. For medium-sized private banks, the cost/income ratio is 84%, around two percentage points higher than in the previous year. Across all private banks operating in Switzerland, the 2020 cost/income ratio (median) rose 6 percentage points to a record high of 85.9%. To be sure, institutions were able to cut costs in travel and marketing. However, the lower operating expenses were unable to offset the decline in income.

"The solid performance of the strong banks in the midst of difficult market and pandemic challenges is a testament to the investments they have made in recent years to strengthen their resilience. They have achieved this by consistently investing in customer acquisition and efficiency," explains Philipp Rickert, Head of Financial Services at KPMG Switzerland. This is also reflected in the institutions' return on equity: While large private banks have a median return on equity of 6.2%, the median for small banks is 1.1%. Overall, the average return on equity (median) was 4.1%, which represents a slight deterioration compared with the previous year (4.2%).

Assets under management and net new money increase

Assets under management increased by 3% to just under CHF 2,943 billion across the private banking sector in 2020. This was mainly due to strong growth in net new money of CHF 94.5 billion (+3.3%) last year, with large private banks in particular attracting a lot of new money. For example, around 95% of net new money was generated by seven of the largest private banks. Overall, 48 banks reported positive net new money and 35 banks reported negative net new money. "The considerable inflow of new money over the past two years is an extremely encouraging sign for the industry and for Switzerland as a leading financial center in private banking," Rickert said. Mergers and acquisitions, on the other hand, did not have a significant impact on private banks' assets under management last year, as some of the announced transactions have not been or will not be completed until 2021.

Only minor cost savings for office space

The 27 executives surveyed last year - mainly CEOs - expected at the time that home offices would benefit banks in terms of office costs and other efficiencies. But as things stand, only limited reductions in office space expenses are evident. Cost savings in the 2020 pandemic year were modest at 0.9%. In contrast, the decrease in travel and marketing expenses led to larger cost savings at most banks, reducing general and administrative expenses by 9% (CHF 388 million).

Executives last year assumed that loan defaults would result in only minor credit losses in 2020. It is true that the industry's credit losses (includes lombard, mortgage and other credit losses) increased more than fourfold year-on-year (from CHF 126 million to CHF 597 million). However, a large part of this is attributable to one bank. Overall, the number of private banks reporting an increase in credit losses in 2020 remained relatively stable at 31. In the previous year, there were still 28 private banks reporting increased credit losses.

Digitization and ESG gain in importance

As the private bank study also shows, private banks want to devote more attention to topics other than the Corona crisis. This includes the entire ESG (Environmental, Social and Governance) area, which is becoming increasingly relevant. Thus, private banks are evolving in the ESG area and adapting their offerings. However, there are big differences between banks. While a majority of 60% of the institutions have ESG listed on their website. Only about 20 financial institutions had it evident in their annual reports or on their websites that ESG is a key strategic priority. "Banks should leverage Switzerland's strong track record of ESG pioneering and investing to attract new generations of clients for whom ESG is a key concern," Rickert said.

The topic of digitization continues to gain in importance. For example, an increase of 327% in keywords relating to digitization has been observed in banks' annual reports over the past ten years. Despite this, private banks made lower IT investments in 2020 and recorded lower IT-related costs than in the previous year. "The lower IT spending is mainly due to banks' reluctance to invest in the crisis year. We expect investments in IT to pick up again, as digital transformation will remain a key issue," explains Hintermann.

Methodology