Probate proceedings: The underestimated instrument

The Corona pandemic is severely restricting economic life in some sectors. More and more companies are in danger of being financially on the brink due to a lack of sales. Experts are accordingly warning of a wave of bankruptcies. But by no means every company would have to be sent into bankruptcy. Depending on the situation, a debt-restructuring moratorium can secure a company's existence.

The consequences of the Corona pandemic are being felt particularly acutely by some sectors, such as the travel, hospitality and events industries. Industry insiders believe that the weeks-long loss of sales will mean "lights out" for some companies unless financial help arrives quickly. In other words, there is a threat of an increase in insolvency proceedings.

Avoid bankruptcy and liquidation thanks to probate proceedings

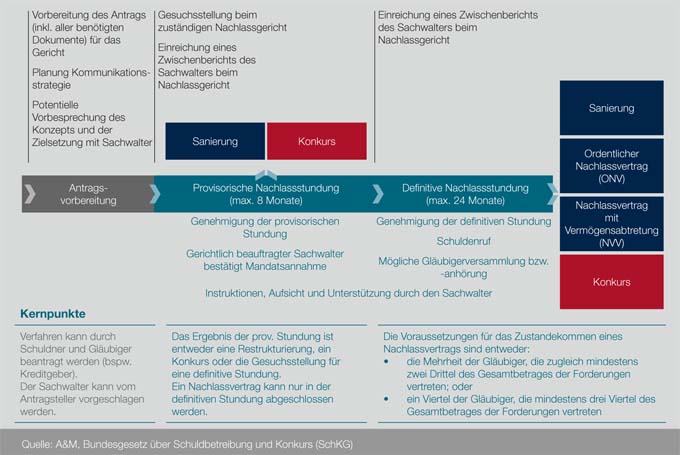

Swiss debt enforcement and bankruptcy law (SchKG) essentially provides for three forms of insolvency proceedings: bankruptcy, composition proceedings or bankruptcy moratorium. Little known and relatively little carried out is the composition procedure. This was the finding of a new study published by the consulting firm Alvarez & Marsal and the Swiss Turnaround Association. The composition procedure according to SchKG must be applied for at a court and has the following effects, among others:

- Debt collection and legal proceedings are suspended

- Assets of the debtor cannot be seized

- Assignments of receivables become ineffective upon approval of deferment

- Statutes of limitations stand still

- As soon as the deferment is granted, interest ceases to accrue against the debtor for all claims not secured by a lien (unless otherwise stipulated in the composition agreement)

- Preventing the cancellation/cancellation of claims prior to the probate proceedings.

- No social plan obligation in case of mass redundancies occurring during the probate proceedings concluded with a probate agreement with assignment of assets

- Appointment of a custodian; with the custodian's consent, long-term contracts can be terminated if they stand in the way of reorganization

The probate process probably could have actually saved some companies that filed for bankruptcy in the recent past - along with many jobs.

Managers should assess the financial situation more objectively

The study found that companies in payment difficulties often wait too long before taking the necessary measures, and when they do, they realize that there is little room for maneuver left and that the company will ultimately have to file for bankruptcy. Instead, in the event of liquidity bottlenecks, company management should objectively evaluate restructuring at an early stage and consider a debt-restructuring moratorium as a possible solution. A debt-restructuring moratorium gives companies the time they need to implement restructuring measures.

Out-of-court solutions are often preferred instead of probate proceedings. In 2019, according to the study by Alvarez & Marsal (A&M), only 66 Swiss companies opted for a debt-restructuring moratorium. Compared with the 4,691 bankruptcies in the same period, the debt-restructuring moratorium instrument was only used in around 1.4% of all Swiss bankruptcies. By comparison, petitions for Chapter 11 proceedings in the USA were ten times higher in 2019 (14%).

40% of companies that went into probate in 2019 were successfully restructured

17 (38%) of the companies that were granted forbearance in 2019 and for which the proceedings are now closed were successfully restructured either through a straight restructuring or through an ordinary forbearance agreement with their creditors. In 28 (62%) of the closed proceedings, the company ceased to exist. Nevertheless, in 5 cases a solution was found, either with a fall-back solution (i.e. the healthy part of the company became an independent entity) or the company was transferred to a third party. According to the study authors, in the current difficult economic environment, debt restructuring could be an excellent tool for rescuing competitive companies suffering from the Covid 19 shock.

In 2020, only 34 companies entered into a debt-restructuring moratorium

In the period from January 2020 to the end of September 2020, 34 companies were granted forbearance. If this number is extrapolated for the year, it corresponds to 45 cases and a decrease of 30% compared to 2019. This decrease can be explained by the Swiss government's COVID-19 support measures for companies. Compared to the 2,760 bankruptcies in the same period, the debt rescheduling instrument was only used in around 1.2% of all bankruptcies.

In addition to the ordinary procedure, only 22 companies used the simplified COVID-19 Probate proceedings. This is a low-cost procedure that was in place until October 19, 2020 to protect small businesses from the COVID-19 shock. This shows that an initial wave of insolvencies was effectively avoided for the time being by the Swiss government's other COVID-19 measures. These measures included government-backed COVID loans, the relaxation of short-time work compensation and the temporary suspension of the notification of over-indebtedness under Art. 725 of the Swiss Code of Obligations (CO).

What are the requirements for probate proceedings

The formal and material requirements for provisional debt-restructuring moratorium are deliberately kept low by the legislator. A provisional restructuring plan must be submitted. However, there are no legal requirements as to what the restructuring plan must contain in the application for debt-restructuring moratorium. In practice, the provisional restructuring plan usually contains an overview of the measures and objectives of the intended restructuring process. An application can only be rejected if there is obviously no prospect of reorganization. In this case, the probate court opens bankruptcy ex officio (Art. 293a SchKG). In practice, the challenges are less apparent in the formal requirements than in the costs involved in a debt-restructuring moratorium, which must, however, be considered in the light of all creditor claims and the loss of jobs.