Private debt financing gains in importance

The volume of the Swiss private debt market is around three billion Swiss francs. In particular, new platform-based business models that involve a variety of different investors offer potential for growth. For the first time, a study conducted by the Lucerne University of Applied Sciences and Arts on behalf of Schwyzer Kantonalbank and Remaco sheds light on this previously little-known market in Switzerland.

The market for non-publicly traded debt financing has gained increased attention in recent years. The Lucerne University of Applied Sciences and Arts examined for the first time

comprehensively and systematically the significance and potential of private debt in Switzerland. For borrowers, private debt represents an alternative source of financing to the classic

bank financing. It is an interesting asset class from the perspective of the money lenders.

What is Private Debt?

The term "private debt" is generally defined in various ways. In the broadest sense, private debt encompasses any debt financing of companies via a non

publicly traded market. This therefore includes, in the broadest sense, all forms of bank loans, loans by non-banks, promissory note loans, special financing,

Consumer loans, private real estate financing, etc. Unlike the public market, private-debt instruments are typically illiquid. Therefore, the lenders intend to

usually to maintain the commitment until the end of the term. Furthermore, there are usually no public market prices for these instruments. Often, the term private debt is understood in a narrower sense and is limited - as also in the context of the study mentioned here - to non-exchange-traded debt financing of companies by non-banks.

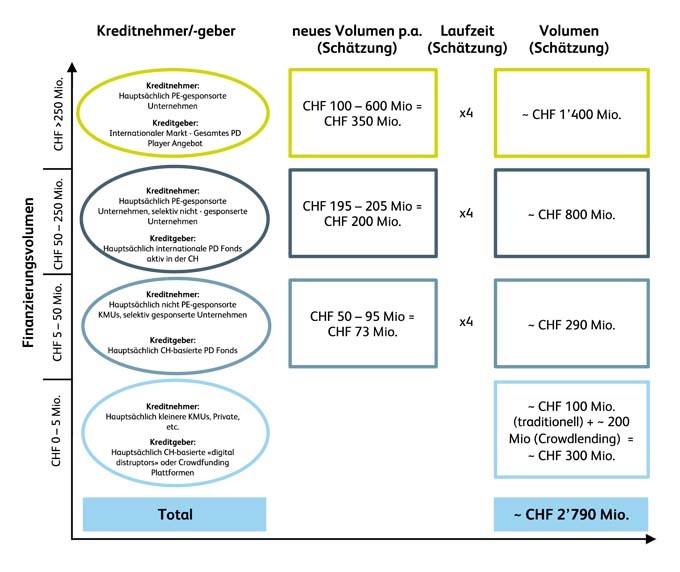

Market volume in Switzerland is around three billion Swiss francs

Number crunching in a non-public market is difficult. Based on numerous interviews with relevant market players, the authors developed a classification of the

Swiss market (see chart). The volume of the private debt market is estimated at around three billion Swiss francs. Individual larger private equity transactions have a strong influence on private debt volumes. However, the authors also observe numerous small transactions, for example in crowdlending, which also contribute to the increase. Internationally, the private debt market is also experiencing high growth. The current volume invested in private debt funds worldwide is estimated at over USD 750 billion. In 2018 alone, it is estimated that more than USD 100 billion in new capital was raised.

Niche market with potential for new business models

Compared with the lending volumes of banks or public debt capital markets, the private debt market in Switzerland continues to operate in a niche. For Thomas K. Birrer, professor at the Lucerne University of Applied Sciences and Arts and co-author of the study, the banks will remain clearly the most important credit providers for Swiss SMEs: "We expect, however, that especially in the case of

Financing via digital platforms continues to show high growth rates. The authors also see great potential in business models that combine the advantages of traditional bank financing with those of online platforms. Such platforms will also enable the inclusion of funds and institutional investors in the financing of loans for companies. Thomas K. Birrer says: "We assume that the diversity of credit offerings for companies in Switzerland will increase.

Willingness to invest in private debt exists

Institutional investors are invested to varying degrees in the private debt asset class and hope, firstly, to achieve higher returns by investing in such assets, secondly, to make good investments in the longer maturity segment and, thirdly, to achieve diversification effects. The good experience to date is also the reason why there is a willingness to increase the allocation to private debt. Nevertheless, as with other investments, the respective risks must be considered and efficient access to suitable investment opportunities must be established.