Customer experience in private pension provision not convincing

According to a survey by the digital agency Namics, many customers are not satisfied with the advice they receive from pension providers. For 42 percent of the customers surveyed, the pension products do not meet their needs.

The full-service digital agency Namics conducted a study on the topic of "Customer Experience in Private Pension Provision - Will Personal Advice Remain Indispensable in the Digital Future?" For the study, the e-business experts evaluated the customer experience when concluding private pension products. The result: the customer experience is only satisfactory and fails to inspire. The most important touchpoint is still the personal consultation, which, however, has a high potential for optimization. More than 800 customers of more than 24 different banks and insurance companies who have taken out private pension plans in the past were surveyed. The companies surveyed include Allianz, Commerzbank, Credit Suisse and PostFinance.

Customer needs: Fear of old-age poverty and lack of individual offers

Financial service providers must understand and be able to respond to the needs and requirements of their customers. The study shows which goals customers pursue with a private pension plan and what the triggers are for dealing with this topic:

Those who define such clear needs also demand correspondingly personalized products. That's why more than 80 percent of respondents want to take out a product that optimally meets their individual needs. However, these products are often missing, as the study shows: 42.0 percent of customers state that their current product is not tailored to their needs.

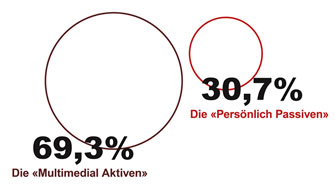

Customer types: Active and passive behavior patterns

The study shows clear differences in customer behavior with regard to interaction with companies. These are particularly evident in the search for information within the customer journey. Two types of behavior can be derived:

The "multimedia active" actively inform themselves via all channels and prepare for a conversation. They are receptive to advertising via both traditional and online channels and need advice as a supplementary touchpoint. The "Personally Passive" hardly inform themselves and expect to receive all information in the consultation. They are not receptive to advertising and must be made aware of the topic by the advisor or by people close to them. Here, too, the consultation is the central touchpoint - this is where all the information is obtained and decisions are made about possible approaches.

Customer Journey: The most important touchpoints and channels from trigger to completion

The two types go through the same customer journey. However, they differ greatly in some cases in their choice of touchpoints and channels. For example, 60.6 percent of the "multimedia active" customers cite online advertising as the trigger for finding out about private pension provision. Among the "Personally Passive," the figure is only 12.9 percent. The choice of touchpoint also differs in the information phase. Whereas 79.8 percent of the "multimedia active" users obtain information from bank and insurance websites, only 19.3 percent of the "personal passive" users use this touchpoint. When it comes to contact, however, both types agree: at over 77 percent, direct contact with the customer advisor is a key channel. Both also agree on the desire for personal advice. When it comes to closing the deal, there is again a serious difference, especially when it comes to sending documents. Here, 52.6 percent of the "multimedia active" are in favor of the online portal, while only 28.2 percent of the other group are.

Customer satisfaction: Enthusiasm looks different

According to the study, the customers surveyed are satisfied overall, but not enthusiastic. This was determined by the Customer Experience Index (CXi), which measures overall customer satisfaction. This shows a solid performance of 72.9 percent for the industry as a whole. In comparison, the perception for insurance companies with a CXi of 75.6 percent is slightly higher than for banks (cf. 68.8 percent). Customers thus experience the conclusion of a private pension product as "moderately positive".

The complete study on customer experience is here available as download.