Tax landscape in Switzerland: profit taxes down slightly

In Switzerland, tax rates for corporate profits and top incomes fell slightly last year. This is shown in a new overview by KPMG. With the introduction of global minimum taxation, there are also signs of a shift from tax competition to subsidy competition to attract or retain companies. This is currently particularly evident in the USA and the EU.

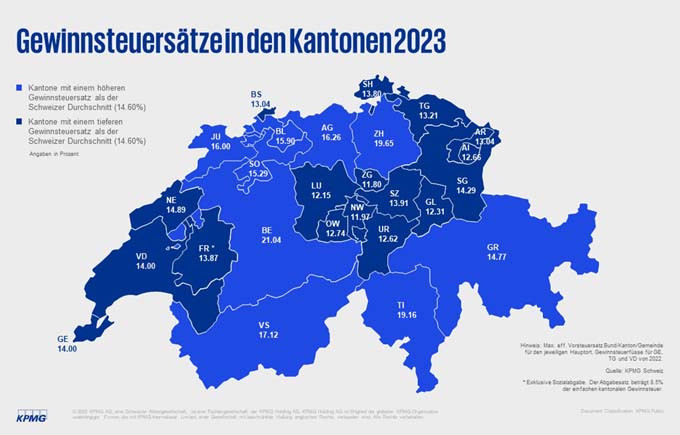

After many rates were reduced in previous years due to the STAF corporate tax reform, there were only isolated, minimal tax rate reductions from 2022 to 2023. The ordinary corporate income tax rates in Switzerland are as follows compared to the previous year slightly - from 14.68% to 14.6%. This is shown by KPMG's "Swiss Tax Report 2023", which compares the profit and income tax rates of over 50 countries and all 26 cantons.

Switzerland's tax landscape: Central Switzerland tops

The largest reductions were made in the cantons of Aargau (-1.16 percentage points) and Basel-Landschaft (-2.07 percentage points). In contrast, the canton of Neuchâtel increased its profit tax rate (+1.32 percentage points). The lowest ordinary profit tax rates continue to exist in the cantons of Central Switzerland, as well as in the cantons of Glarus and Appenzell-Innerrhoden. The canton of Zug leads the ranking of low-tax cantons with a rate of 11.8%, followed by the cantons of Nidwalden (11.97%) and Lucerne (12.15%). The canton of Bern brings up the rear with a profit tax rate of 21.04%. "In the next two years, a further slight decrease is possible, as some cantons will further reduce their tax rates in accordance with the decisions made at the time in the STAF environment. However, individual increases cannot be ruled out either," explains Olivier Eichenberger, corporate tax expert at KPMG.

In an international comparison, Switzerland taxes companies low, especially the cantons of Central Switzerland as well as Basel-Stadt, Geneva and Vaud. Only Guernsey (0.0%), Hungary (9.0%) or Bulgaria (10.0%) offer even lower ordinary profit tax rates. Ireland (12.5%) taxes similarly to Switzerland and thus remains the most important competitor in Europe.

Tax rates for top incomes for private individuals largely unchanged

The average tax rates for private individuals in Switzerland changed minimally compared with previous years on a nationwide average and remained stable at an average maximum tax rate of around 33.45% (-0.07 percentage points). With a tax rate of 22.06 percent, Zug continues to offer the most attractive income taxes in a cantonal comparison, followed by Appenzell Innerrhoden (23.82%), Obwalden (23.3%) and Schwyz (24.98%).

The cantons of western Switzerland, led by Geneva (44.74%), followed by Basel-Landschaft (42.17%) and Vaud (41.5%), continue to bring up the rear. For 2023, the canton of Schaffhausen (29.52%) surprises with 1.22 percentage points lower taxes.

Source: KPMG

Promote non-tax factors

Switzerland would do well to prepare for the coming changes in tax competition, warns the auditing firm KPMG. In order to maintain the attractiveness of the location, further location measures must be introduced or existing ones promoted. "The planned implementation in Switzerland gives the cantons leeway for any location measures with the additional tax revenues," explains Stefan Kuhn, head of tax and legal consulting at KPMG. This is because, according to the federal government's proposal, 75 percent of the income from the supplementary tax is to remain with the cantons, giving them the opportunity to secure and promote location attractiveness for their part. These are supplemented by non-tax factors such as the availability of a skilled workforce, employer-friendly labor laws and competitive income taxes. "When designing new location promotion measures, care must be taken on the one hand to ensure that they have little or no negative impact on minimum taxation. On the other hand, they must be accepted by the OECD and the EU," Olivier Eichenberger, corporate tax expert at KPMG, points out.

If one follows the developments abroad as a consequence of the introduction of the OECD minimum taxation, one notices the trend of a shift from tax competition to subsidy competition. The EU and the USA, for example, have introduced government subsidies aimed at promoting sustainability. The EU's "Green Deal" aims to reduce greenhouse gas emissions by at least 55 percent by the end of 2030. The U.S. Inflation Reduction Act seeks to incentivize greenhouse gas reductions and encourage investment in domestic manufacturing and support for the development and commercialization of new technologies. "In concrete terms, this means for Switzerland that the race for subsidies is already on and the introduction of similar support measures should be discussed now at the latest," says André Güdel, Head of Business Development Tax at KPMG, assessing the situation for Switzerland.