Options for action for SMEs when it comes to pension provision

The figures are impressive: Within the last ten years, the number of pension funds under private law in Switzerland has decreased by one third. This consolidation trend is likely to continue in the coming years. Nevertheless, SMEs have access to various solutions that allow them to specifically map their individual pension needs.

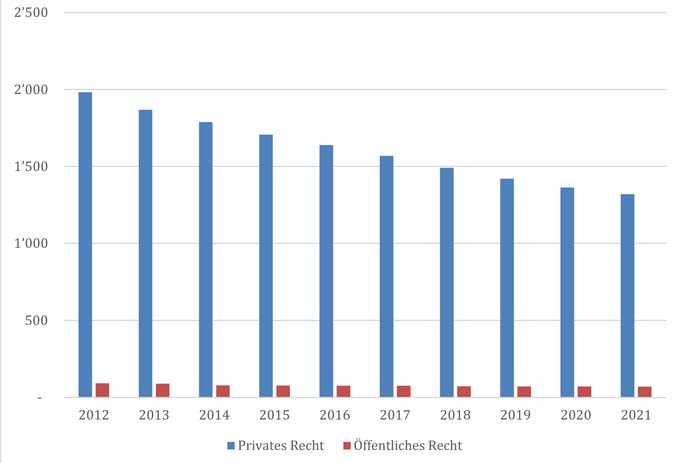

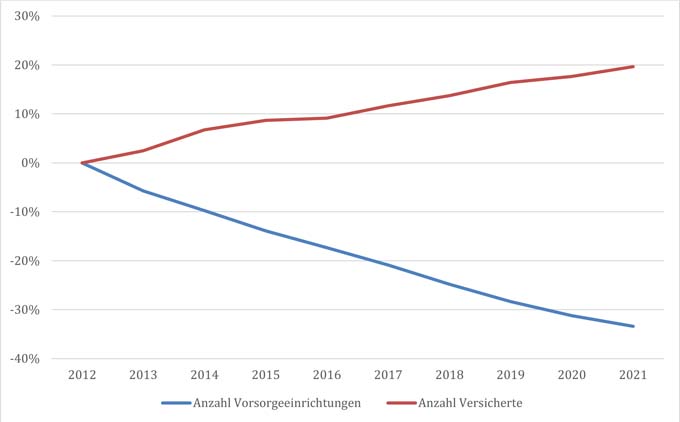

For years now, the number of pension schemes under private law in Switzerland has been falling: according to figures from the Swiss Federal Statistical Office (BfS), there are now 33% fewer pension schemes than in 2012 - at the end of 2021, there were just 1,320, compared with 1,982 ten years earlier. At the same time, the number of insured persons increased by just under 20%. The reasons for this development are complex.

Regulatory requirements increase costs

On the one hand, increasing regulation led to more security, but on the other hand it also increased costs: general administrative costs, asset management, auditing, experts and supervision. The fixed block of costs, which is incurred irrespective of the number of beneficiaries, became larger and accordingly placed a heavier burden on the smaller funds than on the larger ones. The process of BVG structural reform placed greater responsibility on the boards of trustees, making it increasingly difficult for company-owned pension funds to recruit sufficiently qualified representatives of employers and employees as trustees.

Accounting and financial commitments also play an important role. In particular, this concerns provisions and deficit guarantees on the part of the companies, which can entail potential risks. The required provisions to cover future pension payments, for example, are based on assumptions such as life expectancy, investment returns and inflation. In addition, there is the risk of a deficit guarantee on the part of the companies. This means that any gaps in coverage or deficits of the pension fund must be compensated by the company. This represents a financial risk for the company, especially if the pension assets are not sufficient to cover the obligations. On the one hand, possible hedging through reinsurance minimizes the risk, but on the other hand, it increases the costs, which has a greater impact on smaller pension plans in particular because the premiums for this insurance tend to be higher and is therefore not always sufficiently cost-efficient.

High pensioner populations lead to challenges

In addition, demographic developments are contributing to the death of pension funds in the second pillar. Many pension funds have an excessively high number of old people, i.e. too few active insured persons and thus too few contributors in relation to pensioners. As a result, the funds are faced with the challenge that they are writing imputed losses with every pension withdrawal, which calls into question the long-term security of pension benefits. Accordingly, the financial risk is constantly increasing.

Affiliation of one's own pension fund to a collective foundation is one possible solution: it improves financial stability and reduces risks. In this collective model of pension funds, several companies pool their pension funds, distribute the risks, provisions and deficit guarantees among several companies according to the number of beneficiaries, and thus reduce the financial risk for individual companies evenly. In addition, they benefit from economies of scale and pension know-how.

Affiliation with collective foundation or alternative solutions?

However, affiliation with a collective foundation is subject to conditions. In particular, an excessively high pension portfolio cannot be transferred without further ado due to existing regulations for collective foundations. In addition, an affiliation with a collective foundation can dilute one's own funding ratio, although this figure is still much taken into account when it comes to assessing the financial stability of a pension fund. The structure of the assets to be contributed can also be a hurdle, as many pension plans own directly held real estate or other assets that may not be readily available for sale at market price at a given time.

Options that map specific SME pension solutions are offered by Tellco, one of the leading Swiss providers of pension fund solutions. To minimize the complexity and expense of having your own pension fund, for example, management and/or asset management can be contracted out. The managing director of the collective foundation, Janine Hermann, explains: "We have developed a model in which the pension funds continue to enjoy a great deal of decision-making freedom while still benefiting from the advantages of a collective institution." With Tellco pk's Individua solution, the companies determine the asset manager and the custodian bank, they decide on the conversion rate and the technical interest rate as well as the interest on the retirement assets - of course always in compliance with the regulatory and legal provisions. In addition, there are various included auditing mechanisms such as actuarial reports, ALM analyses and investment controlling. The company can act very independently within the shell of the foundation and benefits, for example, from not having to deal with regulatory adjustments.

Individual decision

It should be noted that both individual and collective models have their advantages and disadvantages. Individual pension plans can give companies the greatest control and flexibility under favorable circumstances, but also financial risks if the beneficiary structure is unfavorable or the market environment is difficult. On the other hand, collective models can spread the risk across several companies, but are more limited in terms of individual adjustments and control. However, according to Janine Hermann of Tellco pk, the decisive factor in choosing a model is to think about one's own needs and goals: "What do you want the new model to accomplish? How much decision-making power and responsibility does the future pension fund commission want to exercise? Should there be dilution/cross-funding with other companies or do you want to remain as independent as possible?"

Ultimately, the choice of model depends on various factors such as the size and financial strength of the company, individual needs and risk tolerances. A thorough review before choosing the most appropriate model is of high importance.

This article was written with the kind support of Tellco.